Interest rates are going up, er, no, now rates to remain unchanged, er, no it is up. Inflation has peaked, er, but no, latest data seems to show inflation still festering, so now more upside on rates! This has been the continuous yo-yo effect of quickly digested information we have heard happening around the globe for the past few months now, maybe longer! It all somewhat resembles the Donna Summers hit song which goes “ Upside Down…and round and round!” Showing my age!

The bottom line to this market choppiness and recent weakness is speculation that there may be a further official rate rise in the US and Europe, as well as one in Australia next month. Even though global supply constraints have been steadily improving, we are seeing spending remaining at the high levels for the past year, even still at the very visible higher prices for most goods and services we purchase. I guess that is how business works, put up prices until demand and spending show signs of detracting.

We must be close to that peak point, one would think. Price rises and higher interest rates just do not appear to weary the consumer…yet! In reality though, it must impact soon, one would have to believe, but the concern is that inflation will linger more persistently and longer than the central bank officials and economists anticipated. It seems there has been a constant wave of further price increases in recent months, especially with employment remaining very robust, and spending cash flow flowing. The rising price of oil and gas now is also more in the volatility mix, which unfortunately has been heightened by the latest Middle East flare up.

Global economies still seem to be moving along at fair speed and elevation, albeit within a sub-trend growth trajectory expected for the next few months.

We are in an adjustment period, and things should settle down soon. For this happen, there will probably need to be more stable and normalised inflation and interest rate levels, a sort of self-correcting really. Again, this is in the process of settling, possibly by early 2024, which should see bond and equity markets return to more positive outcomes again for investors. In the meantime, there are long- term bargains for investors to be had in such prevailing market volatility.

We must not forget the core reason why we actually do invest. It is to best secure our financial futures, and deliver consistent and solid income streams of cash flow from our accumulated and diversified investment portfolios, mainly for use in our post-working lives. As investors, we must retain a long-term focus, and realise that with volatility comes many good opportunities to add more investments at decent value prices. We must again remember that we should control what we can control, and we should manage what we cannot control. And to keep the commitment to our goals, and having patience, in the harder more volatile times, are the necessary rudders to future financial success and security.

On this investor characterisation theme, and with the current state of play in the markets, I believe that the article below written by Dr Shane Oliver, Head of Investment Strategy and Chief Economist with AMP Capital, is both very relevant and very accurate in its messages for the true investors, of which we all are and should be. I would recommend you read through this article for its quality of information and the reassurance for investors of the points which the paper details. It is also factual, interesting reading and written with salient quotes too.

Key points in this Dr Oliver’s article, “Three reasons to err on the side of optimism as an investor” , include:

– The natural human tendency to focus on bad news, the increased availability of information and the rise of social media are magnifying perceptions around worries and making it easier to be pessimistic.

– However, to succeed as an investor it makes sense to err on the side of cautious optimism: otherwise, there is no point in investing; growth assets like shares have trended up over the long term; and trying to get the timing right of the 2 or 3 years out of 10 when they fall can be very hard.

Three reasons to err on the side of optimism as an investor.

– Introduction

The “news” as presented to us has always had a negative bent, but one could be forgiven for thinking that it’s become even more negative with constant stories of disasters, conflict, wrongdoing, grievance, and loss. Consistent with this it seems that the worry list for investors is more threatening and confusing. This was an issue prior to coronavirus – with trade wars, social polarisation, tensions with China, worries about job loss from automation and ever-present predictions of a new financial crisis. Since the pandemic higher public debt, inflation, geopolitical tensions, and rising alarm about climate change have added to the worries. These risks cannot be ignored, but it is very easy to slip into a pessimistic perspective regarding the outlook. However, when it comes to investing the historical track record shows that succumbing too much to pessimism does not pay.

Three reasons why worries might seem more worrying.

Some might argue that since the GFC the world has become a more negative place and so gloominess or pessimism is justifiable. But given the events of the last century – ranging from far more deadly pandemics, the Great Depression, several major wars and revolutions, numerous recessions with high unemployment and financial panics – it is doubtful that this is really the case, when viewed in the long- term sweep of history.

There is no denying there are things to worry about at present – notably inflation, political polarisation, less rational policy making and geopolitical tensions – and that these may result in more constrained investment returns. But there is a psychological aspect to this combining with greater access to information and the rise of social media to magnify perceptions around worries. All of which may be adding to a sense of pessimism.

Firstly, our brains are wired in a way that makes us natural receptors of bad news. Humans tend to suffer from a behavioural trait known as “loss aversion” in that a loss in financial wealth is felt much more negatively than the positive impact of the same sized gain. This probably reflects the evolution of the human brain in the Pleistocene age when the key was to avoid being eaten by a sabre-toothed tiger or squashed by a wholly mammoth. This left the human brain hard wired to be on guard against threats and naturally risk averse. So, we are more predisposed to bad news stories as opposed to good. Consequently, bad news and doom and gloom find a more ready market than good news or balanced commentary as it appeals to our instinct to look for risks. Hence the old saying “bad news and pessimism sells”. This is particularly true as bad news shows up as more dramatic whereas good news tends to be incremental. Reports of a plane (or a share market) crash will be far more newsworthy (generating more clicks) than reports of less plane crashes this decade (or a gradual rise in the share market) ever will. As a result, prognosticators of gloom are more likely to be revered as deep thinkers than optimists. As English philosopher and economist John Stuart Mill noted “I have observed that not the man who hopes when others despair, but the man who despairs when others hope, is admired by a large class of persons as a sage.”

Secondly, we are now exposed to more information on everything, including our investments. We can now check facts, analyse things, sound informed easier than ever. But for the most part we have no way of weighing such information and no time to do so. So, it’s often noise. As Frank Zappa noted “Information is not knowledge, knowledge is not wisdom.” This comes with a cost for investors. If we do not have a process to filter it and focus on what matters, we can suffer from information overload. This can be bad for investors as when faced with more (and often bad) news we can freeze up and make the wrong decisions with our investments. Our natural “loss aversion” can combine with what is called the “recency bias” – that sees people give more weight to recent events in assessing the future – to see investors project recent bad news into the future and so sell after a fall. As famed investor Peter Lynch observed “Stock market news has gone from hard to find (in the 1970s and early 1980s), then easy to find (in the late 1980s), then hard to get away from.”

Thirdly, there has

been an explosion in media competing for attention. We are now

bombarded with economic and financial news and opinions with 24/7 coverage by

multiple web sites, subscription services, finance updates, dedicated TV and

online channels, chat rooms and social media. This has been magnified as

everything is now measured with clicks – stories (and reporters) that generate

less clicks do not get a good look in. To get our attention news needs to be

entertaining and, following from our aversion to loss, in competing for our

attention dramatic bad news trumps incremental good news and balanced

commentary. So naturally it seems the bad news is “badder” and the worries more

worrying than ever which adds to a sense of gloom. The political environment

has added to this with politicians more polarised and more willing to scare

voters.

Google the words “the coming financial crisis” and it’s teeming with references

– 270 million search results at present – and as you might expect many of the

titles are alarming:

- “A recession worse than 2008? How to survive and thrive.”

- “Could working from home cause the next financial crisis?”

- “Economic crash is inevitable.”

- “Three men predicted the last financial crisis – what they’re warning of now is terrifying.”

- “How China’s debt problem could trigger a financial crisis.

People have always been making gloomy predictions of “inevitable” and “imminent” economic and/or financial disaster but prior to the information explosion and social media it was much harder to be regularly exposed to such disaster stories. The danger is that the combination of the ramp up in information and opinion, combined with our natural inclination to zoom in on negative news, is making us worse investors: more distracted, pessimistic, jittery, and focused on the short-term.

Three reasons to be optimistic as an investor.

There are 3 good reasons to err on the side of optimism as an investor.

Firstly, without a degree of optimism there is not much point in investing. As the famed value investor Benjamin Graham pointed out: “To be an investor you must be a believer in a better tomorrow.” If you do not believe the bank will look after your deposits, that most borrowers will pay back their debts, that most companies will see rising profits over time supporting a return to investors, that properties will earn rents, etc, then there is no point investing. To be a successful investor you need to have a reasonably favourable view about the future.

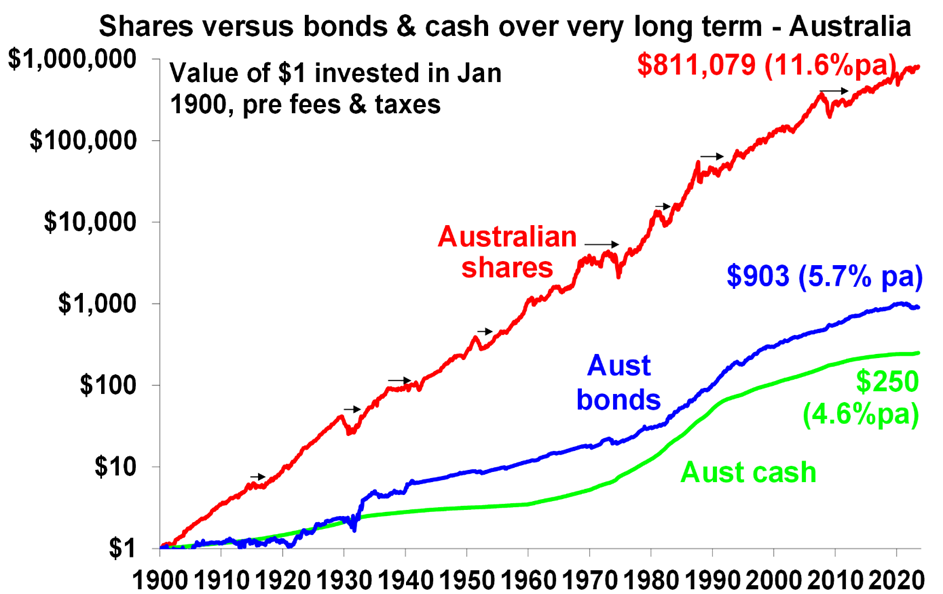

Secondly, the history of share markets (and other growth assets like property) in developed well managed countries with a firm commitment to the rule of law has been one of the triumph of optimists. Sure, share markets go through bear markets and often lengthy periods of weakness – where pessimists get their time in the sun – but the long-term trend has been up, underpinned by the desire of humans to find better ways of doing things resulting in a real growth in living standards. This is indicated in the next chart which tracks the value of $1 invested in Australian shares, bonds, and cash since 1900 with dividends and interest reinvested along the way. Cash is safe and so fine if you are pessimistic but has low returns and that $1 will have only grown to $250 today. Bonds are better and that $1 will have grown to $903. Shares are volatile (and so have rough periods – see the arrows) but if you can look through that they will grow your wealth and that $1 will have grown to $811,079.

Source: ASX, Bloomberg, RBA, AMP

This does not mean blind optimism where you get sucked in with the crowd when it becomes euphoric or into every new whiz bang investment obsession that comes along (like bitcoin or the dot com stocks of the 1990s). If an investment looks too good to be true and the crowd is piling in, then it probably is – particularly if the main reason you are buying in is because of huge recent gains. So, the key is cautious, not blind, optimism.

Finally, even when it might pay to be pessimistic and hence out of the market in corrections and bear markets, trying to get the timing right can be very hard. In hindsight many downswings in markets like the GFC look inevitable and hence forecastable and so it’s natural to think you can anticipate downswings going forward. But trying to time the market – in terms of both getting out ahead of the fall and back in for the recovery – is difficult. A good way to demonstrate this is with a comparison of returns if an investor is fully invested in shares versus missing out on the best (or worst) days. The next chart shows that if you were fully invested in Australian shares from January 1995, you would have returned 9.3%pa (with dividends but not allowing for franking credits, tax, and fees).

Covers Jan 1995 to March 2023. Source: Bloomberg, AMP

If you were pessimistic about the outlook and managed to avoid the 10 worst days (yellow bars), you would have boosted your return to 12.2%pa. And if you avoided the 40 worst days, it would have been boosted to 17.1%pa! But this is very hard, and many investors only get really pessimistic and get out after the bad returns have occurred, just in time to miss some of the best days. For example, if by trying to time the market you miss the 10 best days (blue bars), the return falls to 7.2%pa. If you miss the 40 best days, it drops to just 3%pa.

As Peter Lynch has pointed out “More money has been lost trying to anticipate and protect from corrections than actually in them.”

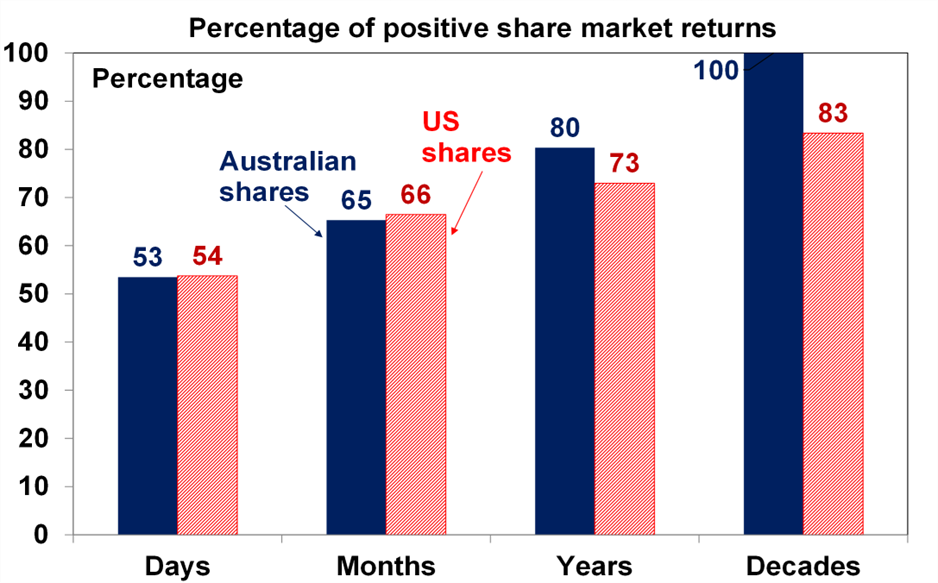

On a day-to-day basis it’s around 50/50 as to whether shares will be up or down, but since 1900 shares in the US have had positive returns around seven years out of ten and in Australia it’s around eight years out of ten.

Daily & monthly data from 1995, data for years & decades from 1900. Source: ASX, Bloomberg, AMP

So, getting too hung up in pessimism on the next crisis that will, on the basis of history, drive the market down in two or three years out of ten may mean that you end up missing out on the seven or eight years out of ten when the share market rises. Here is one final quote to end on.

“No pessimist ever discovered the secrets of the stars, or sailed to an uncharted land, or opened a new heaven to the human spirit.” – Helen Keller.

___________________________________________

As always, should you have any queries please do not hesitate to contact us.

Disclaimer for information provided in this Commentary: This document, and the contents contained within, is a general communication being provided for informational purposes only. It is educational in nature and not designed to be taken as advice or a recommendation for any specific investment product, strategy, or plan feature. The views expressed in this are subject to change at any time. No forecasts are or can be guaranteed.